BIMCO has published the Shipping Overview and Outlook for the First Quarter 2023 (Q1), below we include the highlights of the container, tanker and bulk markets. According to Niels Rasmussen, BIMCO’s Head of Shipping Analytics, the following highlights are the most crucial for each market:

Container market

Q1 2023 Demand recovery from the second half of 2023, but the supply grows significantly faster:

- Significant weakening of the underlying balance between supply and demand with more disadvantages than advantages.

- Freight rates, time charter rates and second ship values all under pressure during 2023 and 2024

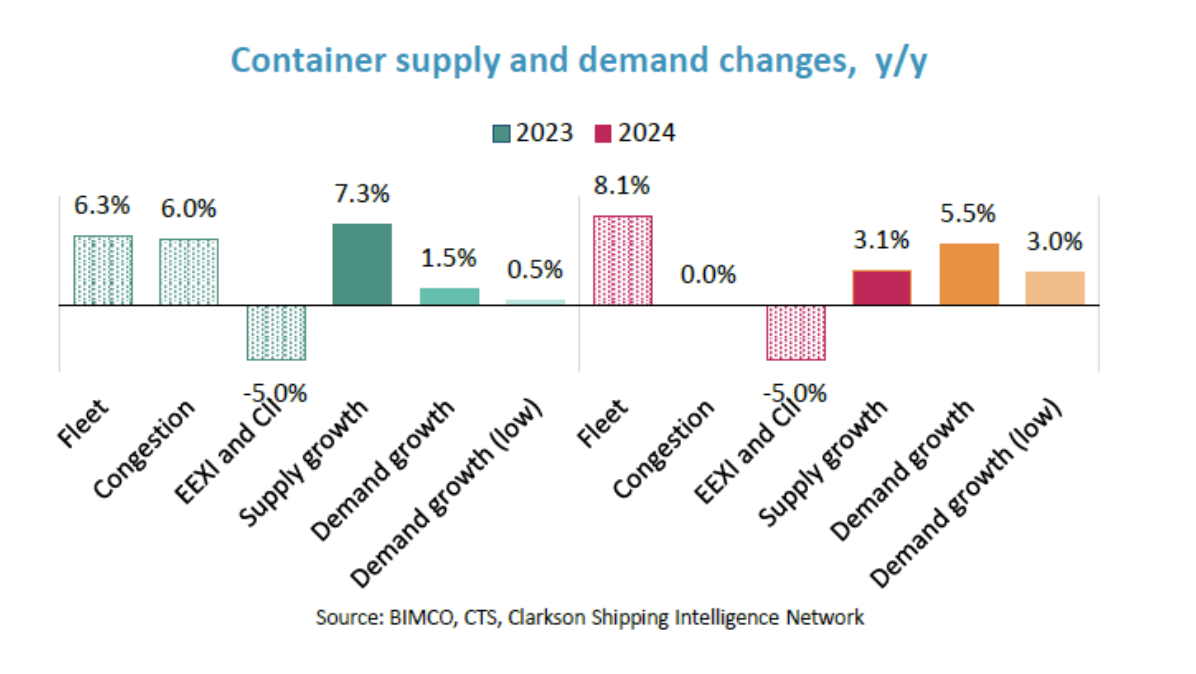

Regional trade and freight transport demand growth of 1-2% in 2023, followed by 5-6% in 2024. - Negative year-over-year growth through first half of 2023, but return to growth thereafter.

- Risks remain and, in our downside case, we estimate growth of 0-1% and 2.5-3.5% in 2023 and 2024, respectively.

- Fleet growth of 6.3% and 8.1% in 2023 and 2024 respectively, while changes in congestion and shipping speed cause supply growth to exceed fleet growth in 2023, but will continue the growth of the fleet in 2024.

- The IMF forecasts world GDP growth of 2.9% in 2023 and 3.1% in 2024, but stresses that the balance of risks remains weighted downward.

- So far, line operators have not been able to adjust the capacity offered according to demand and it is not clear if the published service plans for 2023 sufficiently address this imbalance.

- Although the average speed of navigation has decreased after the reduction of congestion, so far there is no evidence of the downward structural change due to EEXI/CII that had been previously indicated by the main line operators. Therefore, we predict that the changes will be phased in during 2023 and 2024.

![Cambios en la oferta y demanda de contenedores año a año Fuente: BIMCO]()

More info: BIMCO-Shipping-Market-Overview-Outlook-Q1-2023-Container-2023_03

Tanker market

The stars align to create the strongest market in 15 years:

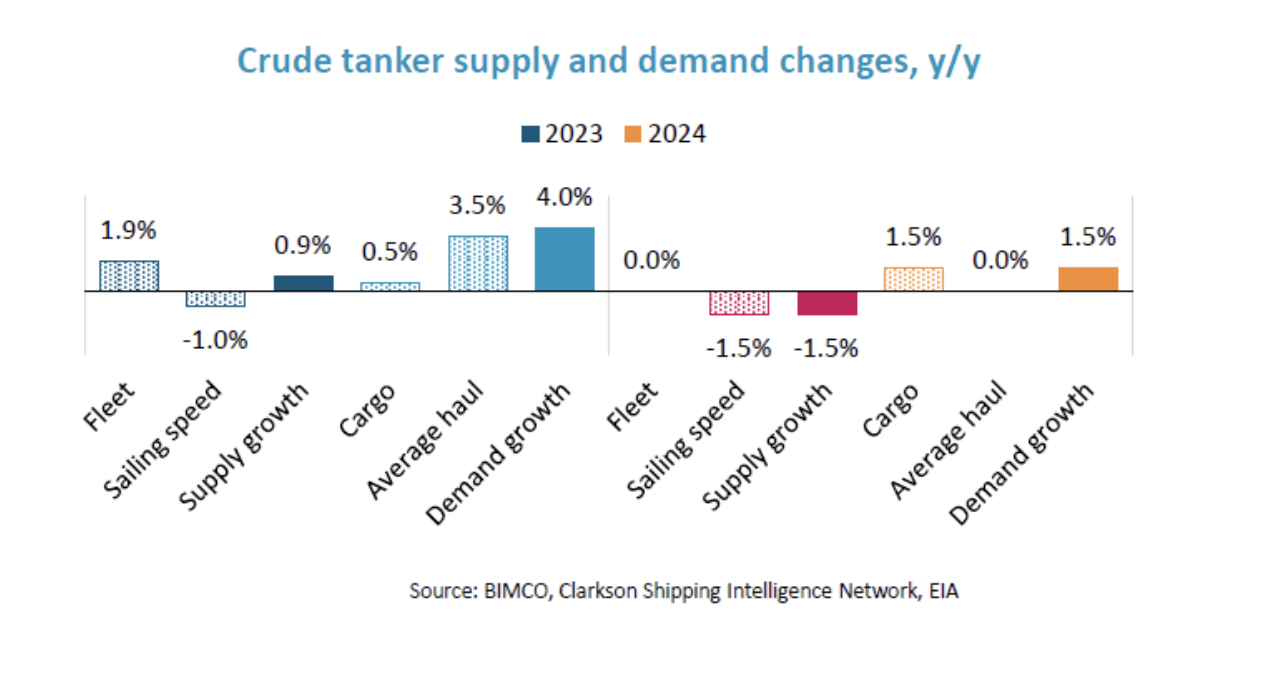

- Demand will grow faster than supply during 2023 and 2024.

- In 2024, we forecast crude tanker demand to increase by 4.5-6.5% over 2022, while supply will decline by 0.6%. Similarly, we forecast product tanker demand growth of 6% to 8%, with supply falling 0.7%.

- Freight rates, time charter rates and second ship values will see gains throughout 2023 and 2024.

- Renewed growth in China and increased demand for jet fuel following the reopening of travel to and from China are key drivers of cargo demand growth.

- Additionally, we expect a 3-4% increase in average sailing distances following the EU ban on Russian oil and oil products will add to tonne mile demand.

- Fleet growth is limited by very small order books. Combined with the expected reduction in browsing speeds of 2-3%% due to decarbonization regulations, overall supply will fall.

- The EIA expects oil prices to fall throughout 2023 and 2024 and Brent to fall below $80/barrel in 2024.

- The IMF forecasts world GDP growth of 2.9% in 2023 and 3.1% in 2024, but stresses that the balance of risks remains weighted downward.

- Therefore, risks to our forecast remain. Cargo demand would suffer from lower economic growth and the expected structural changes have yet to be seen.

More info: BIMCO-Shipping-Market-Overview-Outlook-Q1-2023-Tanker-2023_03

Bulk market

This is how China goes, this is how the market goes:

- We expect demand growth in the range of 1.5-2.5% in 2023, driven by China’s economic recovery.

- Improvements in consumer confidence should help resolve the country’s housing crisis and boost massive demand.

- However, demand growth could weaken to 1-2% in 2024 due to an expected reduction in coal shipments. Import demand should fall as India and China continue to boost domestic mining and

- Europe moves away from fossil fuels.

- The International Monetary Fund (IMF) estimates global economic growth of 2.9% in 2023 and 3.1% in 2024. The Chinese economy is now estimated to grow by 5.2% in 2023, an increase of 0.8 percentage points from the previous IMF forecast.

- The dry bulk fleet is forecast to grow 2.7% in 2023 and 2.0% in 2024.

- Deliveries remain limited amid a small order book of 7.5% of the fleet.

- It is estimated that the offer will grow 0.5-1.5% less than the fleet in 2023 and 2024 due to lower speeds caused by compliance with EEXI and CII regulations.

- The supply/demand balance should improve in 2023, although risks will remain in 2024.

- We expect rates to start to recover as demand picks up in China.

- Capesize ships should benefit from a recovery in iron ore demand, while Panamax ships are more exposed to a drop in coal transport.

More info: BIMCO-Shipping-Market-Overview-Outlook-Q1-2023-Bulk-2023_03

Fuente: Safety4Sea

Source

Safety4Sea