Seasonal norms blunt recent improvements in freight markets

Slipping truckload demand obfuscates capacity exits

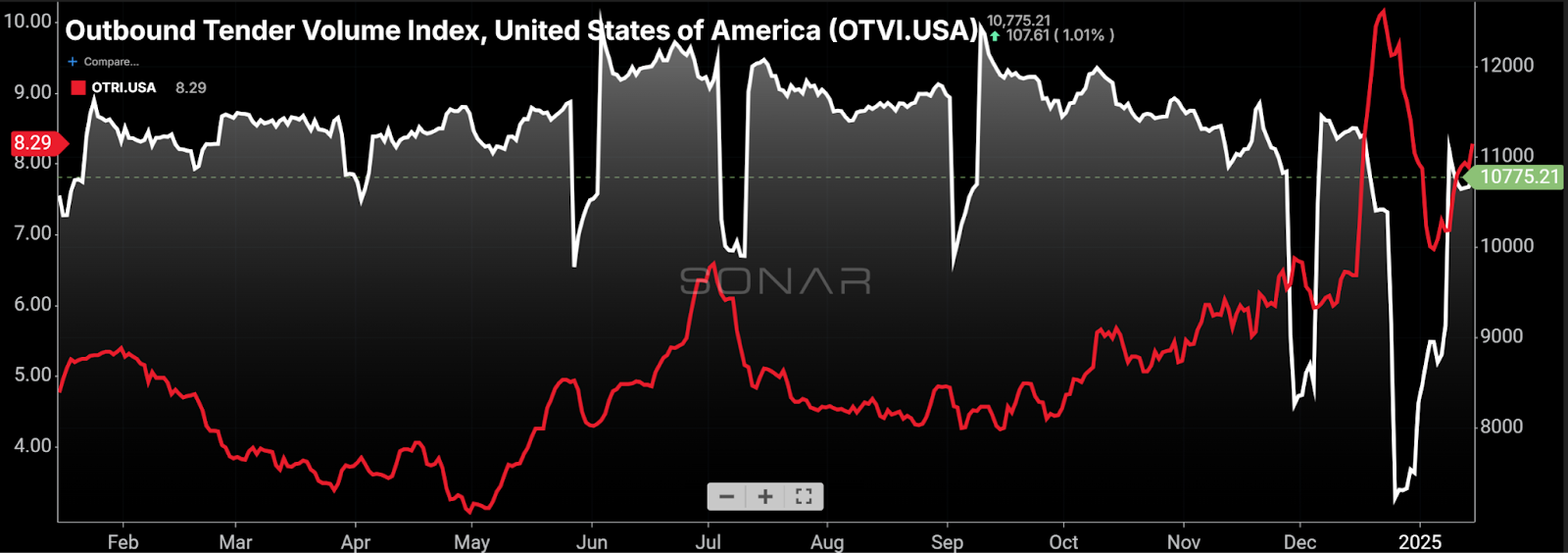

Carriers have been rejecting more tenders the past few months, but the change would have been much greater if not for lackluster volume. (Chart: SONAR)

SONAR’s primary measure of volume, the national Outbound Tender Volume Index (OTVI), which measures total shipper requests to carriers, is down 2%, year over year. Weather and the timing of holidays make clean comparisons difficult this early in the year, but volume softness appears to be preventing tender rejection rates and spot rates from rising further. Yet, both of those metrics are higher year over year, suggesting the recent trend in the direction of tightening is primarily, if not entirely, capacity-driven. With those data points in mind, we could see a much greater increase in tender rejection rates and spot rates when we get into a seasonally stronger period of the year, which normally begins in March.

Container ship lines in no hurry to return to Red Sea

A recent FreightWaves article explains why ocean carriers are still avoiding the Red Sea: The effective capacity that has been removed as a result of longer routings greatly boosted carriers’ profits. In fact, China-owned Cosco reported that its earnings before interest and taxes increased 91% year over year in 2024 on only moderate growth in cargo volume. Avoiding the Red Sea was far from the only source of operational disruption in the maritime industry last year – throughput was also impaired by port congestion (notably at the Port of Singapore) and scarcity of oceangoing containers that arose midyear.

Trans-Pacific eastbound spot rates from Ch…

CONTINUE READING THE ARTICLE FROM FreightWaves HERE

Comments are closed, but trackbacks and pingbacks are open.