LTL pricing discipline may not hold, report says

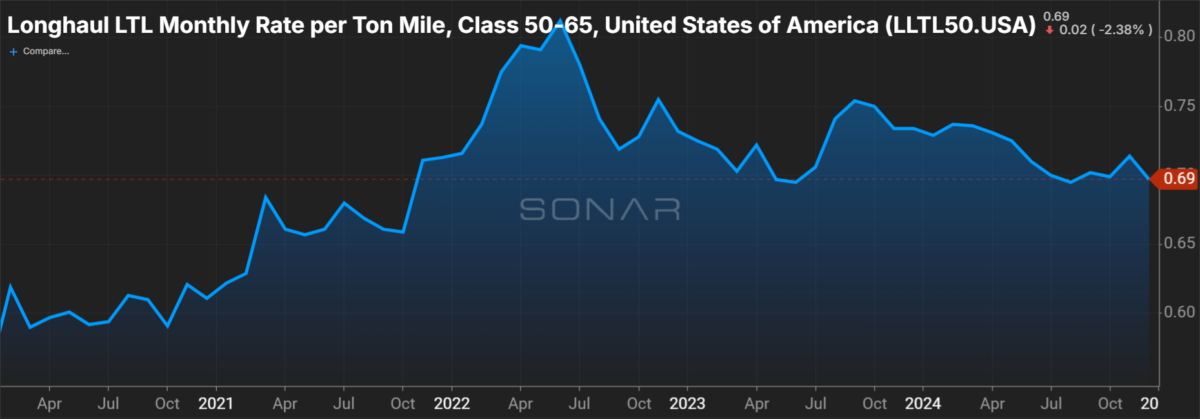

Less-than-truckload pricing appears in need of the next catalyst, according to a report from 3PL AFS Logistics and financial services firm TD Cowen. The update classified LTL rates as steady but noted “some indication carrier pricing discipline may start to crack” as demand remains tepid.

The industry got a reprieve from the freight recession in the summer of 2023 when the nation’s third-largest LTL carrier, Yellow Corp. (OTC: YELLQ), shut down. With the industrial economy in its third year of a downturn and no major carrier on the brink of closure, the LTL industry will likely need a more meaningful demand catalyst to continue to push rates higher.

The TD Cowen/AFS Freight Index shows the LTL-rate-per-pound dataset was 62.7% higher in the fourth quarter than its January 2018 baseline. That was 140 basis points higher year over year but 140 bps lower than the third quarter. The index is expected to record a fifth consecutive y/y increase in the first quarter (to 62.4% from 61% a year ago) but will be down slightly sequentially – typical for the seasonally slowest quarter of the year.

“LTL pricing has been resilient, and a major factor is the increased sophistication of carriers and their ability to price freight in a way that is closely tied to the true cost to move it,” said Aaron LaGanke, vice president of freight services at AFS, in the report. “But there are opportunities for shippers, especially as low demand persists and carriers seek out ‘attractive’ freight they can move efficiently.”

With a finite number of carriers in most regions, the LTL industry is much more disciplined on pricing than the highly fragmented truckload space, which has an abundance of carriers willing to take noncompensatory rates during downturns. However, volume is needed at some point to keep LTL pricing momentum going.

Fourth-quarter updates from publicly traded LTL carriers showed gross yields (revenue per hundredweight inclusive of fuel surcharges) were slightly negative on a y/y comparison but up by low-single-digit percentages excluding fuel surcharges. LTL carrier margins traditionally benefit from higher fuel prices because fuel surcharge mechanisms move higher as the per-gallon price increases.

CONTINUE READING THE ARTICLE FROM FreightWaves HERE

Comments are closed, but trackbacks and pingbacks are open.